Everi - EVRI trade idea

Sector: Consumer Discretionary

Industry: Services - Miscellaneous amusement & recreation business

Introduction

My thesis starts by searching for a stock that is not affected by commodity prices.

Of course, just because is not affected by commodity prices does not make it a good buy, this is why I choose a stock in an industry that is growing very fast.

Everi Holdings Inc. provides entertainment and technology solutions for the casino, interactive, and gaming industries in the United States, Europe, Canada, the Caribbean, Central America, and Asia. It operates in two segments, Games and FinTech.

They are in a very good position to take advantage of digital acceleration and adoption.

Multiple growth drivers, but the main ones are multiple games integration and cashless experience.

Users are not just more familiar with cashless systems, but they prefer it.

Everi offers cashless experience integrations services and the growth is very robust. They are live with 7 of 11 operators. Basically, they have very good growth with only 7 operators, more room to grow on the operator's side.

As they mention in the last earnings call, the operators are still thinking in a short time horizon about their investments until they have more clarity from the public officials.

In the next period is very likely that we will see all operators being live and also prepared to make investments in digital improvements. The company leadership wants to remain conservative about the growth outlook, but in my opinion, the growth trend will not end any time soon.

In the earnings call quotes, you have more details about the growth drivers.

The stock has rallied very strong from Mar 2020 until today, I am aware of that. Now the question is "the rally will continue?".

Financial Highlights

Everi Holdings Inc. - Q1 2021 Earnings Call

C. Michael Rumbolz

On a consolidated basis, our revenue set first quarter record and reflecting our improved margins, we set all-time quarterly records in net income, adjusted EBITDA and free cash flow. In fact, operating income was up 55% over the first quarter of 2019, while our adjusted EBITDA was up 23% over the then record 2019 first quarter. On an operational basis, our outstanding performance is reflective of a variety of factors and these are some of the examples. The complementary balance between our games and FinTech segments has never been stronger. Our focus on developing innovative price has resulted in an increasing demand from customers since our products help them build stronger relationships with their patrons, and at the same time, improves their operating efficiencies. Also, we have developed a track record of consistent operating execution that gives our customers confidence that we deliver the products and services that they expect. And finally, and most importantly, our worldwide Everi team whose commitment to collaboration and excellence has made all of this happen.

Randy Taylor

Thank you, Mike, and hello, everyone. We hope you are all doing well. While our core recurring business operations are providing strong growth and profitability in today's environment, we continue to invest to ensure the sustainability of our growth. Our R&D investments are focused on promoting internal development and product enhancements that will drive ongoing longer-term organic growth. As the year progresses and business volumes continue to recover, we also expect that operating expenses will begin to increase as normal business activities resume and we incur more of the marketing and other costs that support our customer relationships. However, I'll highlight that as a percentage of total revenue, we do expect total expenses will trend lower than pre-pandemic levels, thus supporting some margin improvement as compared to prior years.

Another growth driver comes through expanding the number of games available to iGaming operators. We can draw upon our large library of successful land-based casino games while also leveraging our development of new land-based player popular games by adapting them for the online world. One added focus is creating customized games for our operators, which strengthens our relationship with some of the country's fastest-growing I-game operators. Another very exciting opportunity is the significant interest in the commercial and travel casino operators in our cashless, enterprise-wide mobile wallet, our digital CashClub Wallet. Importantly, for operators, our CashClub Wallet platform is fully customizable to meet their different needs and can be white labeled to carry each casino's own branding. With our flexible system, operators can choose the level of experience they want to offer their patrons and the speed at which they move forward. We believe we are at the very beginning of a significant transition that will enable our customer to deliver an integrated digital cashless experience alongside existing cash solutions.

For operators with online offerings, such as iGaming and sports wagering, CashClub Wallet also provides funding to bridge a patron's online experience with their land-based experience. Our solution complements our financial access services and it's fully integrated with our loyalty and reg tech offerings. It is the next step towards offering convenience for players and significant cost efficiencies for operators. CashClub Wallet fits seamlessly into casinos’ existing back-of-house processes and controls and meets the needs of the relevant banking and other financial regulators at the state and federal level as well as the extensive need of gaming regulators.

In addition to the cost efficiencies that come from reducing the need for cash, operators also see significant advantages in the data and intelligence gathered on their patrons spending across the casino property through our wallet. It provides operators with the opportunity to extend their relationship and connection time with their guests through integration with our player loyalty applications. We believe we are truly at the forefront of the convergence of financial access services and loyalty in the digital casino world. With the stringent compliance requirements that we meet and our history of player funding capabilities, we offer the industry a truly differentiated high-value solution. We are seeing substantial interest by operators, and the initial response from casino's patrons has been positive. Based upon the initial transaction activity from the casino's patrons, our expectation remains that cashless transactions will increase the total number of transactions performed by patrons, providing another growth driver for Everi in the years ahead. However, given the early stage of deployment, we are not yet at a point where it's appropriate to share specific data and project future growth potential. As our cashless solutions go live at additional casinos in the upcoming months and the user base expands, we expect to share further insights about these trends with you.

Mark Labay

Thanks, Randy. Before discussing our outlook, I'd like to provide some thoughts on a significant increase in our free cash flow, and how we're looking at our capital structure. Our free cash flow more than doubled compared to the year ago period. That was essentially equal to the free cash we generated in all of 2019. This growth represents a significant flow-through of the record adjusted EBITDA we earned in the first quarter. The reported free cash flow also benefited from a more modest level of capital expenditures in the quarter. This free cash improves our balance sheet by further bolstering our near-term liquidity. The uncertainty surrounding the recovery of the macroeconomic environment and our industry continues to diminish, this added liquidity may ultimately position us to reduce our leverage more quickly than we had originally expected. While the pandemic may have slowed our momentum towards reducing leverage in 2020, it did not change our goal of reducing total borrowings and achieving lower net leverage ratio.

Turning to our outlook for adjusted EBITDA. Throughout the first quarter, casino activity has clearly increased. To frame out the puts and takes of the macro revenue drivers, our first quarter results likely benefited from rising vaccination rates across the U.S., limitations on casino capacity easing, and casino activity picking up due to pent-up demand. As a result, our first quarter results likely receded added benefit that we might not continue to see as competition increases for consumers’ discretionary dollars from the reopening of other entertainment options throughout the year. With some customers still impacted by some degree of capacity restrictions, or like those in Canada and other international markets where the casinos are still closed, we do believe there is still an opportunity for further recovery. However, in our discussions with customers, many still remain in capital conservation mode. Their capital spending plans are focused on the next 60 to 90 days instead of through year-end. Given this wide range of variable revenue drivers and our outlook that operating expenses will begin to increase throughout the year as operations continue to return to more normalized levels, we believe the second quarter adjusted EBITDA will remain well ahead of the second quarter of 2019.

It could be comparable to slightly below our first quarter 2021 performance. We expect free cash flow will remain strong. But with our semi-annual interest payments on our notes due in June and an expectation for increasing capital expenditures, this should be less than the record $43.5 million generated in the first quarter. We do not expect a further significant ramp in quarterly performance in the back half of the year, without a corresponding and sustained improvement in the overall gaming industry. With competing choices for entertainment dollars becoming more available, we believe a more gradual industry coverage is likely, as more of the population becomes vaccinated, and some of the typical demographics that make up the larger portion of our customers' best players return to their favorite casinos. With that being said and barring any further macro setbacks, we would expect our adjusted EBITDA in the second half of the year will exceed the then record results we reported in the second half of 2019.

Darren D. Simmons

Yes. I think maybe, David, easy way to think of it is, obviously, today our revenues are transactional, right? So there's transactional fees that are garnered through the transactions that we support, whether that be the cash dispensing transactions or the other cash advance transactions. So as we move towards digital, right, this to us is just another transaction type that's got transaction fees associated with it. So it does come with obviously a premium from that standpoint, but also we've got software associated -- sort of software modules associated with it and annualized support. But remember also we're connecting this into other components of the FinTech business and other products. So it's just not a one-trick pony, okay? This is integrated into loyalty. It's integrated to compliance products. So a lot of that kind of goes along into these discussions. So it's just not binary in terms of, "Oh, you're now transacting through a digital wallet." No, no, no. There's other components that are contributing to the revenue opportunity for us.So we see increased transaction volume as we pivot towards digital wallets. And then as Randy mentioned, we are introducing new transaction types associated with the wallet. So we expect that we monetize those as well. So right now we've got transaction fee associated with funds coming in as we bring money into the operator, but we also are giving the opportunity for players to bring money out of the ecosystem and put it back into their bank accounts if they've had it in their wallet. And so there's fees associated with that also. So greater transaction volume and new transaction types that we support and then other products and services that we'll be able to include as a part of the service that we provide as it relates to our wallet, including loyalty and compliance.

Dean Ehrlich

I don't know if I could top what you just put out there, Mike. When your premium installed base grows that substantially over the last couple of years and you continue to perform in a variety of product categories that we have out there, to me it's sustainable. We got 5 different product categories in the premium sector between Flex Fusion or Skyline Revolve or DCX or Arena or even Renegade at this point. And we just launched a latest theme, Press Your Luck. It's done really, really well. We have a lot of areas to turn to that can continue to sustainability, so I'm very comfortable with our product breadth in terms of covering each of those categories. Obviously, you just got to continue to hit the dates on roll out the products that we expect to roll out and we should be looking pretty good.

Noticeable news after the earnings call

Everi Holdings pops as analysts back upside from refinancing

Conclusion

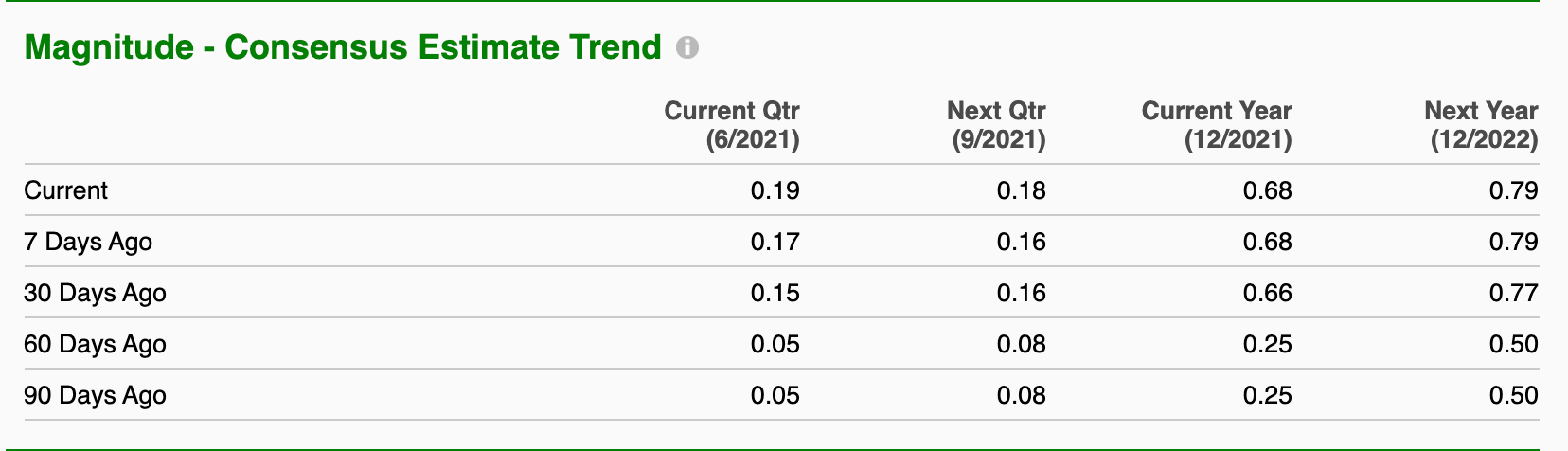

The growth has legs and this is reflected in the consensus estimate trend.

Even if the stock has rallied very hard, I still want to participate in this growth story. At some point, the growth will slow down, but until then, I'm in.

Keep in mind I have a 2 - 6 months time horizon for all my trades.

Disclosure: I have a position in Everi Holdings Inc.

The chart image is for visualization purposes. Is not for timing the entry/exit positions.